Further thoughts and corrections for $TBPH

What if we had an NRI working in nOH

What if I told you the main study scaring investors away is actually riddled with errors, holds surprisingly positive implications for ampreloxetine, and the stock’s dreaded mid-term downside is effectively an upside?

The following article reflects my personal opinion and is not meant to persuade anyone, hence the reasoning might be superficial in some places.

Downside

I’ll admit, in my previous analysis, I was a bit lazy. I did some handwaving to get to that $16.13 per share ($823M) valuation by simply aggregating the $393M pro-forma cash balance (bridging the Q3 $333M balance with $75M in milestones and a $15M burn), $150M in “tail” milestones, and a rough $280M estimate for our 35% YUPELRI interest using 2x peak sales figures.

But if we want a clearer picture of the “floor” in a CYPRESS trial failure, we need to get more into the details.

The Strategic Liquidation Case

TBPH has no active pipeline outside of ampreloxetine and has established a “strategic review board”—the strongest bio corporate speak for a liquidation I have seen. I could give a list of other anecdotal evidence why this is the case, but nothing conclusive, so I will not waste either of our time to persuade readers about a liquidation in case of a failure.

A traditional buyout is unlikely because an acquisition would trigger IRS Section 382, capping the usage of their nearly $1 billion in NOL carryforwards and destroying their NPV. Instead, the most tax-efficient path is to sell assets and wind down operations.

YUPELRI

The strength of the YUPELRI franchise’s patents is underestimated by the sell side (no revenue modeled after 2035).

While key patents expire in 2035, Viatris has settled with major generic manufacturers to keep them off the market until April 2039, showcasing the strength of the patents. This effectively neuters remaining challengers like Mankind Pharma.

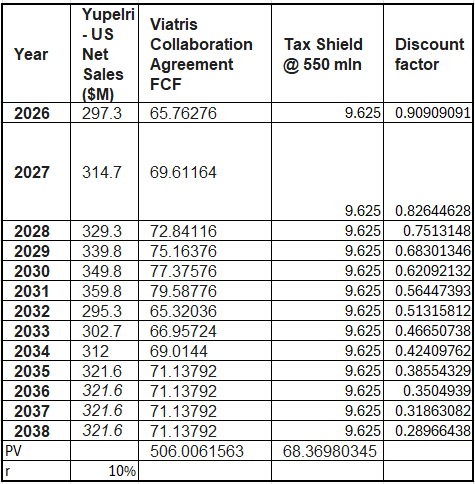

Consequently, I’ve extended the consensus sales through 2038.

Tax Shield and margins

Acquiring an asset provides a tax shield through amortization. While acquirers often seek accelerated schedules to boost NPV, I’ve modeled a conservative straight-line amortization based on a $550 million asset value.

While the value of a tax shield is technically circular (increasing as the sale price rises) assuming a static $550M valuation provides a robust floor. Because of the $1 billion NOL, TBPH won’t pay taxes on the gain between book and market value during liquidation.

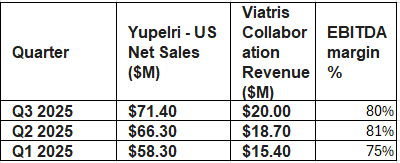

EBITDA margins are also really healthy due to Viatris’s highly efficient distribution network — another fact that might throw off lazy sales-based multiple valuers like me.

The New Bottom Line

When you run the numbers on this “winding down” scenario:

Pro-forma Cash & Near-term Milestones: ~$393M

Trelegy/Viatris Milestone “Tail”: ~$150M

Updated YUPELRI Asset Value + Tax Shield: ~$550M

Total Fair Value: $1.093 Billion

Price Per Share: $21.43

This isn’t a Waiting for Godot trade where you’re praying for the market to wake up. Once the company announces official plans to liquidate assets —which could come down as soon as a trial fail, the stock could bounce back to the $18-19 level promptly.

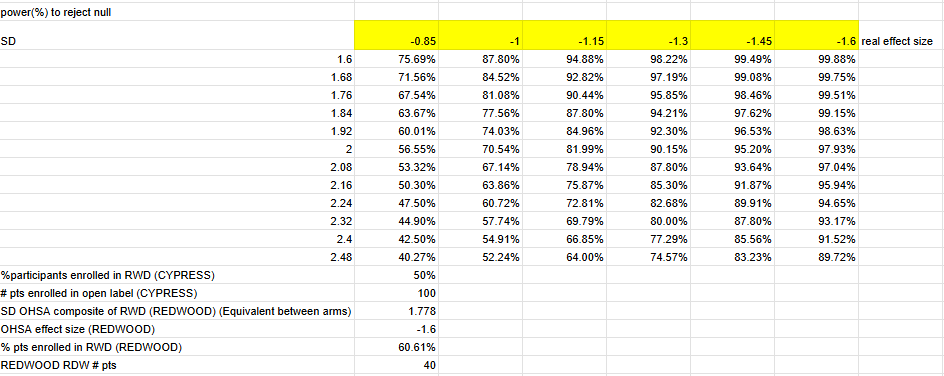

Powering

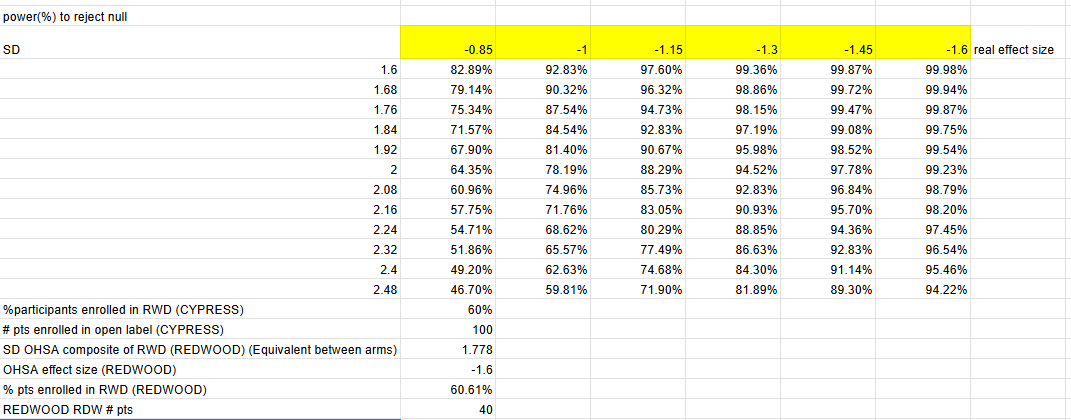

I used Z distribution instead of a t distribution, but at n=30 per arm the real results are relatively close. I am confident-ish that this is really close to the study’s actual powering since management guided that CYPRESS is 90% power to detect MCID change (-1 OHSA point) with variability observed in previous study (Roughly 1.74 single arm SD assuming equal variance between arms).

Theravance could have gotten lucky with the variance decrease at week 22, and the single arm SD could easily be in the 2.4 range based on week 20, in which case the powering would be a coin flip (60% power) at a 1 point OHSA decrease.

Many have raised “redflags” around the fact that the company is unwilling to share how many patients have enrolled into the withdrawal phase, and hence, the powering of the study could be impaired significantly.

I think it is perfectly rational for the company not to disclose how many people enrolled in the withdrawal phase, as it would have implications for market size. As the company has failed its previous study, it is just natural that fewer people would meet the highly placebo-prone enrollment criteria of a 2-point OHSA improvement. This might actually be positive to the company, as this time we might have a larger share of people with real hemodynamic improvement enrolling. If the drug gets approved, the lower enrollment in CYPRESS would have no relevance on the commercial potential as many more people would meet the enrollment criteria.

There is a good chance that enrollment was higher than initially planned, as enrollment was pushed from the end of 2024 to late summer by mgmt in the 2025 Q1 earnings call. Whether a protocol amendment was needed, I do not know, but I believe a sample size modification due to lower than expected people reaching enrichment is a perfectly legit criteria to modify n in the eyes of the FDA.

Alternatively, increased enrollment might not have been needed, as the open-label extension trial has a week 0 visit — or at least the previous one had — so management is able to access pre-withdrawal scores and post withdrawal scores, providing them with the necessary information to keep the powering at an adequate level. Regardless of whether management has access to patient-level or only pooled data, my point still stands.

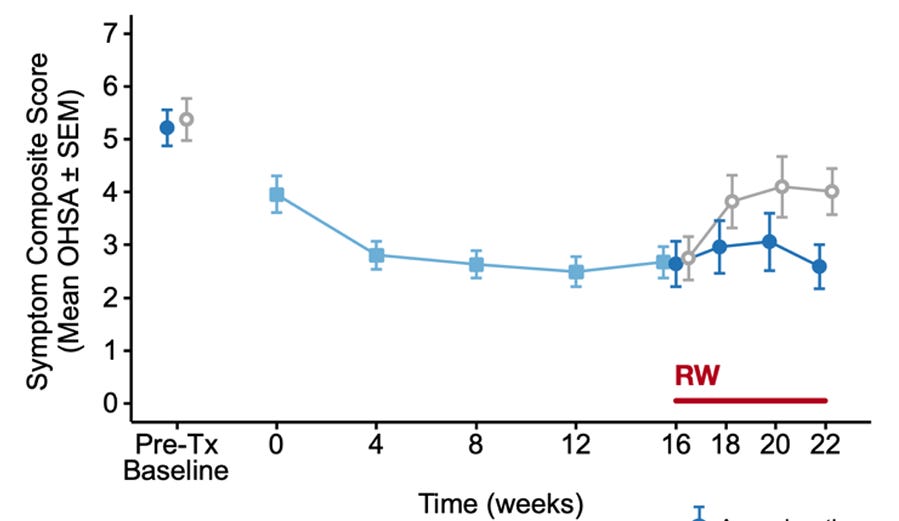

Atomoxetine

To gain a mechanistic understanding of ampreloxetine’s prospects, we can study not just pyridostigmine, but atomoxetine — another NRI —as well.

While many studies show that atomoxetine causes a pressor effect in patients with alpha-synucleopathies (acutely at least), especially in MSA, there is a glaring elephant in the room that darkens ampreloxetine’s prospects: a “failed” randomised double blind crossover study with enrichment.

I believe this study prevented many from getting into this name, but on a closer look, one can discover that the reported statistical figures were miscalculated, and recalculating the significance, we get stat sig results on many of the endpoints!

Let’s dive into how the study is not comparable to CYPRESS and what the problems are with the statistical analyses and the data.

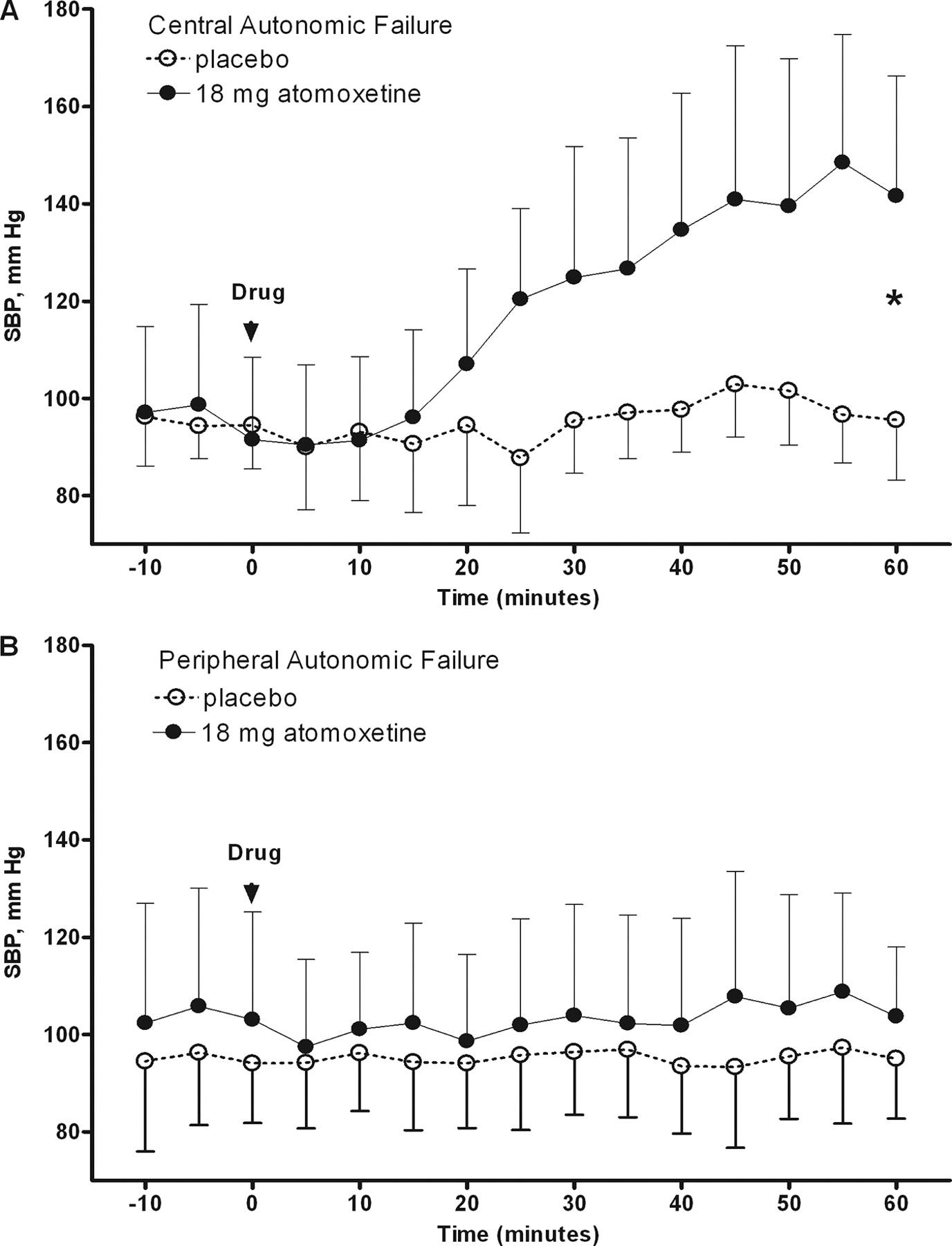

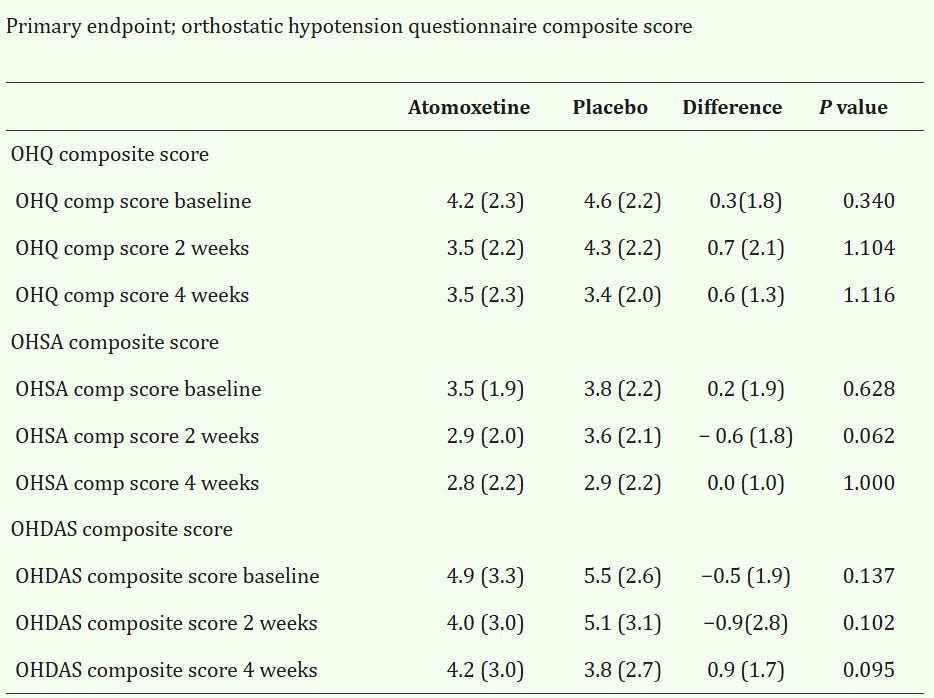

The enrichment criteria was defined by a minimum 10 mmHg increase in standing systolic blood pressure and at least a 1-point (2 for CYPRESS) improvement in the OHSA dizziness score following a single 10 or 18 mg dose (pediatric doses) measured at 1 hour after administration (t_max).

This seems awfully similar to our design, so let us review:

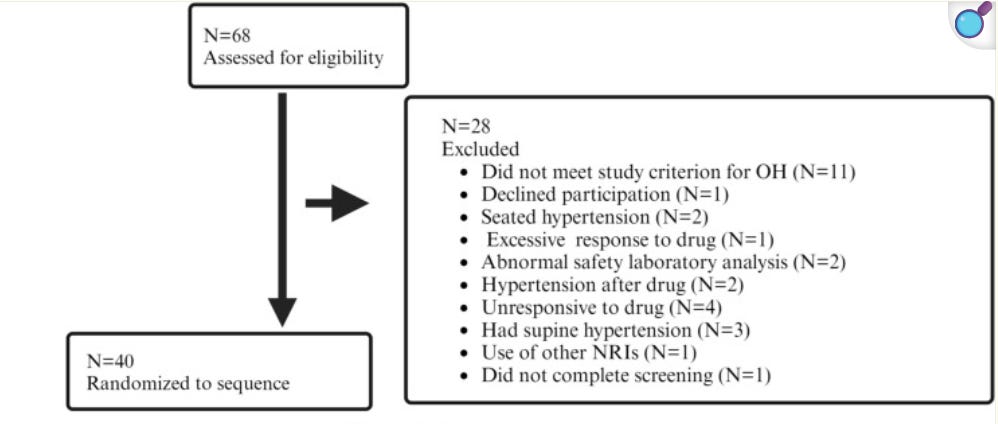

So the enrichment criteria filtered out a grand total of 4 people for not responding to the drug, and 2 for hypertension after the drug, so roughly 40 of the 46 people (only these 2 criteria were a reason for exclusion after drug administration) had advanced to enrichment vs our 60% (or 50% in CYPRESS). Overall fair to say not a very rigorous enrichment.

The study found OHQ scores were so egregious that p-values were greater than 1 —maybe the drug just straight up makes the heads of patients explode.

I remember being taught in 6th grade that probability is a measure that can take on values between 0 and 1, and after 10 minutes of consulting with Gemini, those boundaries still hold, but I am open to learn how one might get p-values larger than 1.

That is not all: Since it was a crossover study with minimal dropout (3/40), the differences column should roughly equal the difference between the atomoxetine and placebo arm (especially since “Only participants who completed the full protocol were included in the final analysis”, so any model induced differences are also off the table), which was not the case at the week 4 endpoints in any of the cases.

Also, the signs just randomly flip, with positive signalling lower scores in the atomoxetine arm, while in some endpoints, the opposite is true.

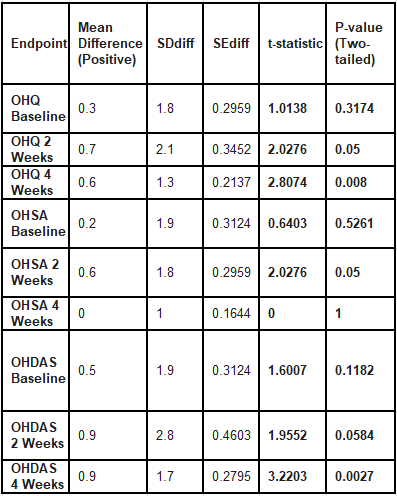

Running a paired sample t-test on the difference scores does yield statistically significant results on many of the endpoints.

Although this data looks phenomenal, I would be wary of drawing any conclusions from it. First, we do not know whether the displayed differences or the placebo-atomoxetine are the true means, and there is evidence that suggests data may have been misrecorded, in which case we can trust neither of the differences.

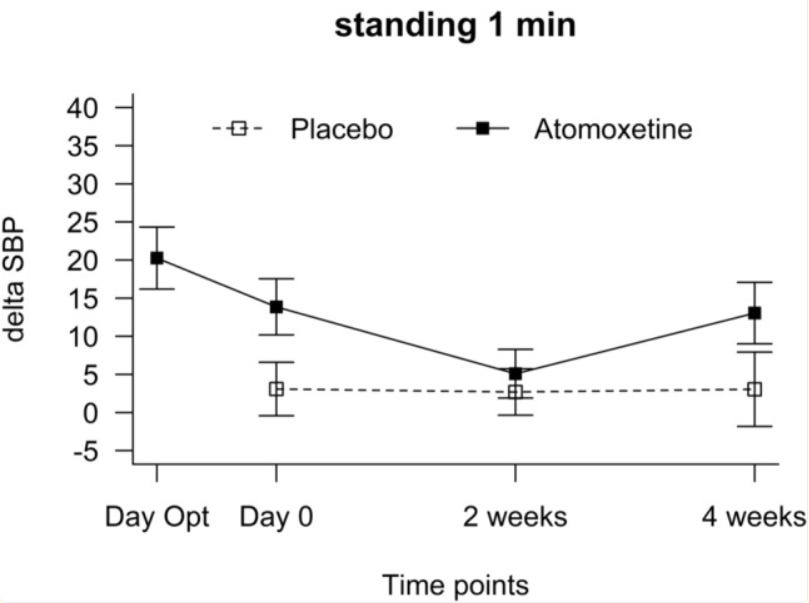

For placebo, the standing blood pressure does not change across treatment compared to baseline (no treatment), or at least not to a a +-0.5 mmHg degree which I can measure using Canva. Interestingly enough, the variance does change.

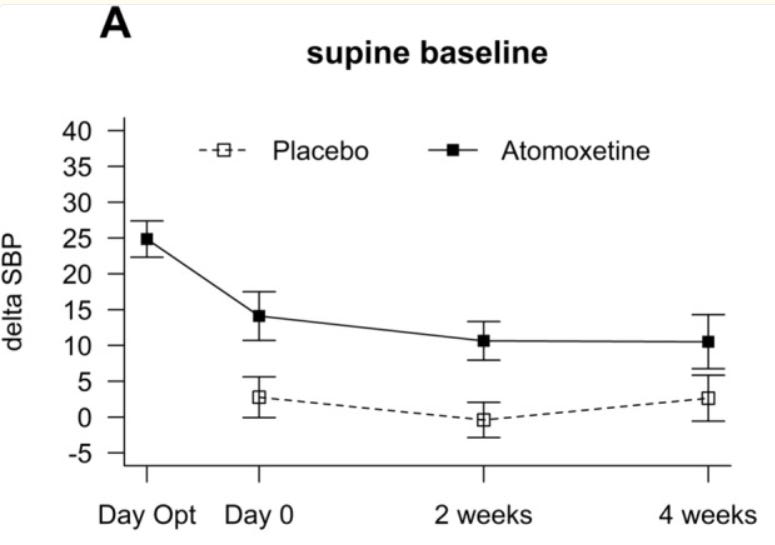

In contrast, the supine baseline does change to a significant degree. The standing delta SBP is highly reminiscent of the OHSA week 4 composite score, where the mean disappears, and SD is exactly 1 — and although they do apply rounding, these 2 figures paired with each other scream error to me.

Conclusion

Bottom line is based on the totality of data, I would argue the trial has a slightly positive readthrough for ampreloxetine. I have contacted the researchers regarding my concerns with the discrepancies in the data. If anyone more expreienced was to review the study, I would love to chat.

We had lplv more than 104 days ago based on the November 10th PR, and earnings is supposedly comes at February 25th (but nothing official yet as forecasts are #working days estimates), I would expect them to share results during earnings.

Disclosure

Not investment advice. The article represents my own opinion solely.