Corbus Pharmaceuticals

The most asymmetric ASCO play

Corbus Pharmaceuticals ($CRBP) will soon present at ASCO with the abstract becoming available on Thursday 5 PM ET. The market seemingly believes that Corbus’s Nectin-4 ADC will have to go head to head with peto and other next generation EGFRs in HNSCC. Based on monolithic data CRB-701’s chances look weak. There is strong readthrough evidence however that 701 will excel in HPV+ HNSCC subsegment which is the exact weak point of EGFR theraphies. The ASCO will show us mature stratified data and will provide rationale to continue development in oropharyngeal squamous cell carcinoma (which is largely HPV +). With cash at $7.38 per share downside is limited, making this a highly asymmetric readout.

HNSCC types

While the broader HNSCC market is becoming increasingly crowded with next-generation EGFR therapies, the oropharyngeal squamous cell carcinoma (OPSCC) is driven by completely different axes than the rest of HNSCC.

Accounting for roughly 30% to 40% of all HNSCC cases, OPSCC is predominantly driven by HPV. This viral driver alters the tumor’s surface profile: research demonstratess that Nectin-4 is significantly upregulated in HPV-positive patients (although Nectin-4 levels are not predictive of response to Nectin 4 ADCs), whereas EGFR expression is heavily downregulated.

This creates the perfect target population for the Nectin-4 ADC, CRB-701. In the US alone, the frontline addressable market for HPV-driven OPSCC is approximately 5,200 patients, with an additional 3,100 patients in the second-line setting, making 2L close to a $1 billion TAM (based on what I believe the duration of therapy will be).

Most of the developers of next-generation EGFR bispecifics do understand this weakness of their assets, as their pivotal trial designs either structurally lock out HPV-positive patients or expose severe clinical weakness in that subsegment. Bicara Therapeutics, evaluating the EGFR x TGF-β bispecific ficerafusp alfa (BCA101), has explicitly restricted enrollment in its pivotal Phase 3 FORTIFI-HN01 trial to HPV-negative patients; any participant presenting with an oropharyngeal tumor must have documented HPV-negative disease to enter. Similarly, Johnson & Johnson is advancing its EGFR x MET bispecific amivantamab in the Phase 3 OrigAMI-5 study, which strictly mandates that any p16 or HPV DNA testing must be negative, completely walling off the HPV-positive market.

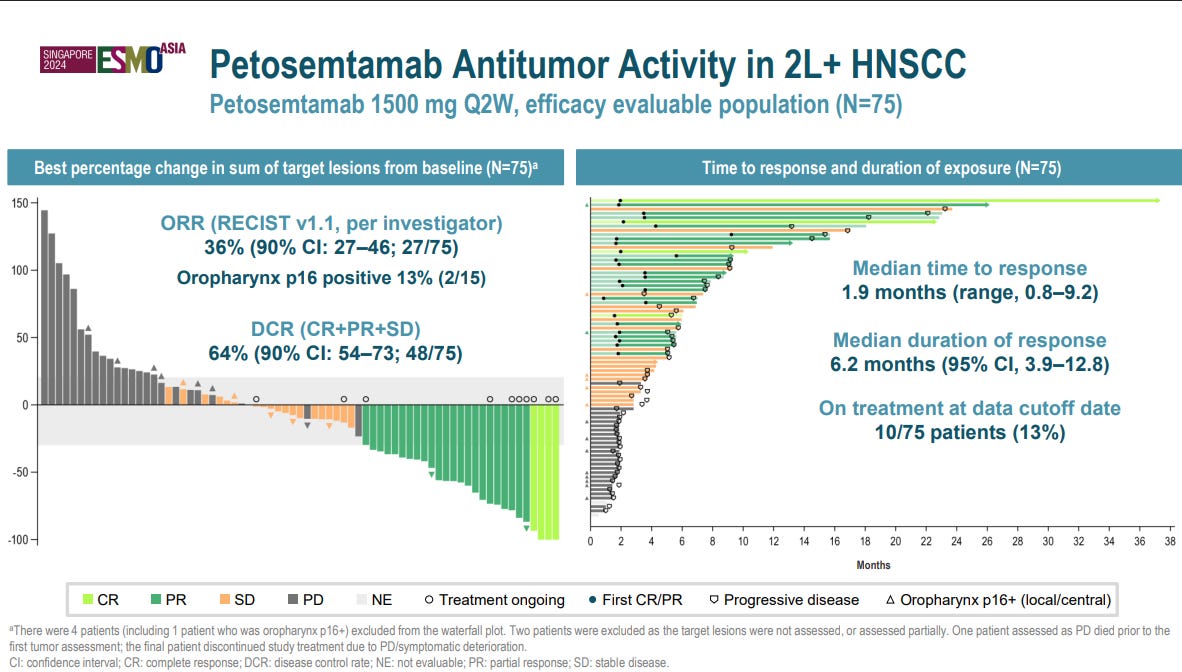

Genmab and Merus’s petosemtamab (EGFR x LGR5) is the sole next-generation EGFR agent pursuing an all-comers approach, allowing both HPV-negative and HPV-positive patients into its pivotal Phase 3 LiGeR-HN1 (first-line) and LiGeR-HN2 (second-line) trials. Recent clinical readouts for petosemtamab revealed the reason why others are not pursing this segment, posting just a 13% overall response rate in its HPV-positive subgroup compared to a competitive 36% in the broad population.

I believe that Merus’ decision to push forward in this category has lead to the anxiety surrounding 701. I do not know whether Merus would be required to publish stratified data, but pooled data wouldn’t necessarily look bad as pembro excels in HPV +, making it harder for 701 to capture the HPV + population if approved.

At ASCO we will get a mature dataset with data stratified by HPV status. As a note, abstract will be boring with the exciting data presented during the poster/oral presentations.

Based on the public comments of the CEO he is highly confident that the data will justify development in OPSCC – note that this is not purely HPV driven, but management likely wants to get a broader label.

We already have Padcev + Pembro 1L data in HNSCC, which give us an idea of how our mono will do in 2L (we have 2L pembro combo data coming Q1 27). The CEO has extensively mentioned this trial which is negative in a sense that it makes it likely to be priced in, but also will lend more credibility if results are repeated making it look less like a post hoc spin.

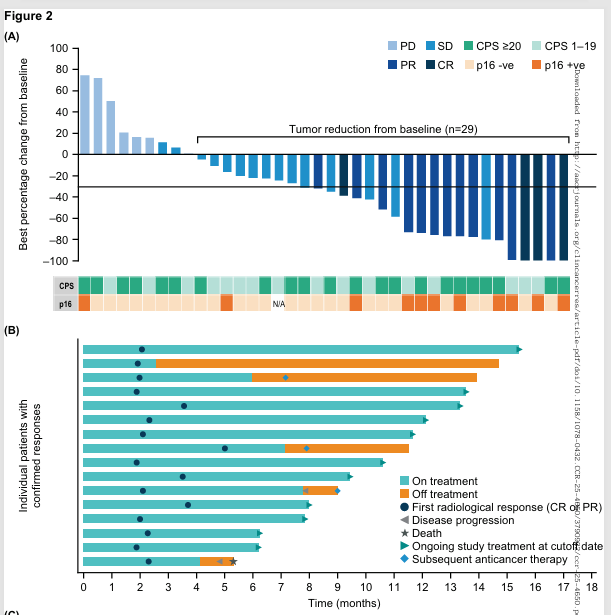

P16+ ve status seems clearly indicative of deep responses, with 9/11 patients The duration of response also seems highly encouraging.

As per the researchers’ words: “While only 11 patients had p16-positive oropharyngeal cancer, they had a cORR of 81.8%, in contrast to 23.3% in patients with non HPV-associated disease which may have driven the cORR observed in the overall population.”

While there was no direct pembro comparator arm, so we do not know what % did pembro contribute according to the authors: “While any cross-study comparisons should be interpreted cautiously, in the present study, the cORR was greater than what was observed with pembrolizumab monotherapy (17%) and similar to what was observed with pembrolizumab and chemotherapy (36.0%) in historical controls “ So we can safely agree that pembro did not do all the lifting here.

But what if pembro’s effect comes completely from the HPV + and hence the 81% ORR in that segment.

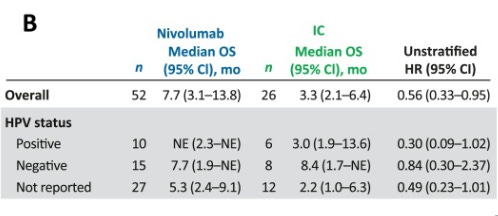

As per Roof et al: “In a phase I study, KEYNOTE-012, patients with R/M HPV-positive HNSCC demonstrated a higher ORR with pembrolizumab alone as first-line or later treatment when compared directly with the HPV-negative cohort (25% versus 14%). Later data from an expansion cohort of KEYNOTE-012 demonstrated an even more pronounced ORR benefit (32% versus 14%), which also translated into an improvement in progression-free survival (PFS) (37% versus 20%) and overall survival (OS) (70% versus 56%) in those patients with HPV-positive disease . However, this finding was not proven in large randomized phase III studies”

I do not think we can arrive at a definitive conclusion effect size attributable to Padcev in the combo study in hpv + based on the evidence presented above, but is clearly at least 3x more effective in this subsegment as Pembro mono would be in terms of ORR.

There has been concerns about durability as the ESMO data shown 58 HNSCC patients 5 who had PR already had PD in the immature dataset, but hopefully those appeared in HPV- cases — the most likely case given the depth of HPV + responses in the padcev combo study.

.

Bar is not high for 2L in terms of durability however for the HPV + population, as in Checkmate 141 which was conducted in 2L with the same comparator arm we would need to be using only achieved a mOS of 3 months which we clearly exceed (a similarly heavily pretreated population as the current mono trial).

My greatest concern is Pfizer, as they discontinued the development of their PD L1 ADC which was being evaluated in HNSCC, which probably explains why Pfizer did not push into 1L after the data immediately. I do not personally buy the toxicity argument as the discontinuation did seem under control. Yes 701 is superior, but we would need to run a H2H which is the exact reason 701 is not being developed in urotherial.

Fully diluted sharecount is 18,706,622 with cash at 138.2 mil at the end of Q1, putting cash at $7.38 per share making downside limited.

Yes, I did not mention the cervical and obesity opportunity, which could provide additional upside on top of 1L/2L OPSCC